Mortgage Backed Securities – what are they and why do we hold them?

Rumi Mahmood

19 August 20204 min

With yields on government bonds reaching all-time lows in recent weeks, we’ve added US Agency mortgage backed securities to our portfolios to further diversify our fixed income exposure.

While many UK investors will be less familiar with the idea of mortgage backed securities, the mortgage market is a major part of the global bond market, accounting for around 10% of the Barclays Global Aggregate bond universe.. In the US bond market, they play an even bigger role, accounting for over 25% of the investment grade universe, not far behind the share of high-grade corporate bonds.

How do they work?

- When a homeowner takes out a mortgage the lender owns the debt – therefore the lender has money tied up in physical asset class form, in this case property.

- In order to free up this capital and reduce its risk, the lender “pools” many mortgages together and sells on the debt to other investors, who in turn earn interest on the loans for the remainder of their duration.

- The lender continues to service the loans but has freed the tied–up capital in this way. Mortgage customers continue to pay the lender, but other investors now own the debt.

This process of “securitisation” enables investors to benefit from the mortgage business without ever having to buy or sell an actual home loan. Typical buyers of these securities include institutional, corporate and, of course, individual investors.

But not all MBS are created equal

There are two general types of MBS: those pooled and managed by quasi-government agencies (Agency MBS) and those pooled by non-government agencies (Non-agency MBS). The former of these two is a central pillar of the US bond market, comprising 30% of all US debt¹.

The Agency MBS market is large and highly liquid, with $8.9 trillion in assets outstanding (as of July 20) and an average daily trading volume of $230 billion based on the average calculated from trade association SIFMA’s data. US agency mortgage debt is assigned the same credit rating as US government debt and is known as US government sponsored – meaning mortgage backed securities are either backed by the full faith and credit of the US government (GNMA), which guarantees that investors receive timely payments, or they have special authority that allows them to borrow from the US Treasury (FNMA, FHLMC)². There are also different grades of MBS depending on the credit-worthiness of the collective borrowers in the pool. The highest quality MBS investments are known as ‘AAA’ (triple A) rated.

Mortgage backed securities are often associated with the global financial crisis that originated in 2007 due to the housing issues the US economy faced at the time. After the housing crisis, the US government increased regulation across several key areas making MBS stringently scrutinised and more robust as an investment, which now requires detailed transparency and disclosures to investors.

Why are mortgage backed securities attractive?

Attractive Yields

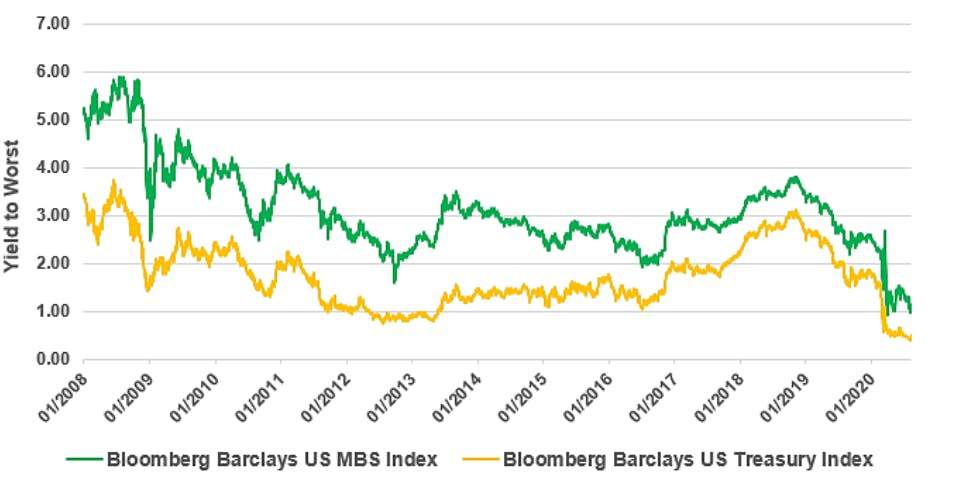

Historically, MBS have offered attractive yields relative to US treasuries. Over the last 10 years, MBS yields have averaged 2.8%, while Treasury bills have averaged 1.6%³ (Figure 1). With US treasuries and UK gilts offering yields close to their all-time lows, MBS offer an attractive yield without increasing credit risk.

Fig. 1 – Attractive Yields – US MBS vs. Treasuries

Source: Bloomberg 2020

Lower Volatility

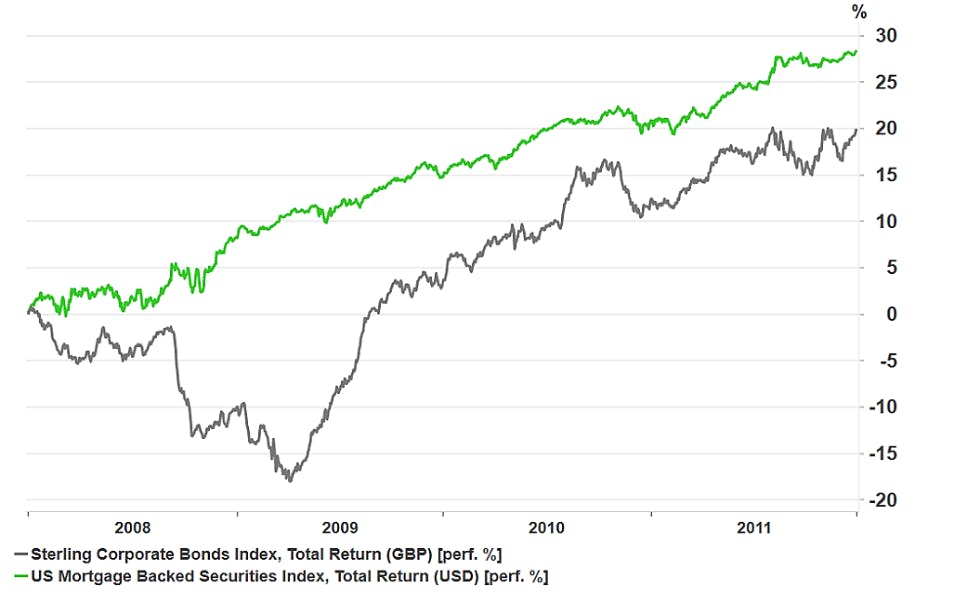

Higher yields have also come with low volatility historically, comparable with other fixed income asset classes. Even during the years of the credit crisis, broadly 2008–2011, MBS were actually a less volatile asset than UK corporate bonds (Figure 2). The standard deviation, or degree of variability of returns for MBS has historically been comparable with US and UK government bonds, in other words providing similar volatility but for higher yields.

Fig. 2- Performance of US MBS and UK Corporate Bonds 2008-11

Source: Bloomberg 2020

Risk adjusted returns

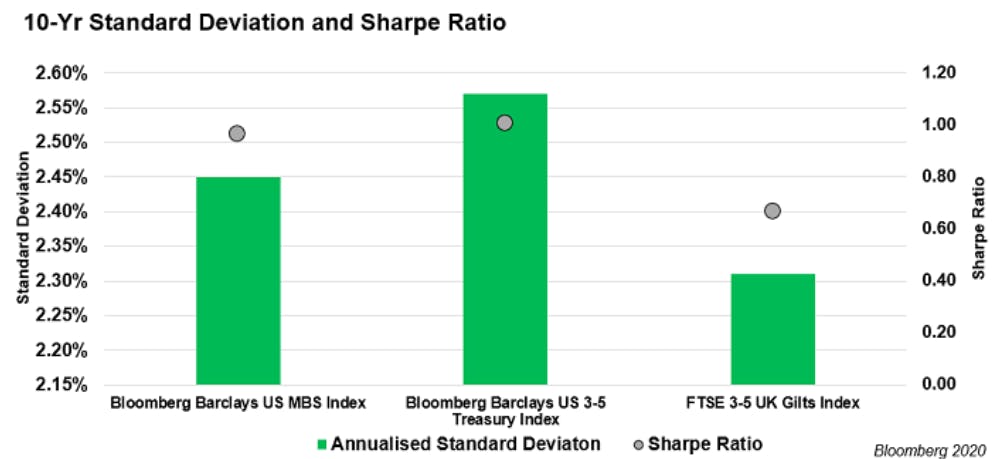

Sharpe ratio is the measure of return achieved per unit of risk undertaken. The higher the figure the better, meaning that investors receive more return relative to the level of risk they take. The risk adjusted return, or Sharpe ratio for MBS has historically been similar to comparable treasuries and higher than gilts, meaning that investors have received more bang for their buck – more return for the same level of risk in MBS versus UK short dated government bonds (Figure 3).

Fig. 3- 10-Yr Standard Deviation and Sharpe Ratio

Source: Bloomberg 2020

Nutmeg portfolios

We believe agency mortgage backed securities are an attractive asset class at the current time, given the extremely low levels of government bond yields. Historically, MBS have also performed well relative to government bonds in stages of the economic cycle where interest rates are stable or rising slowly – something we expect to be the case in the immediate future.

To access this asset class, we’ve used the iShares US Mortgage Backed Securities UCITS ETF, which provides exposure to the higher quality ‘AAA’ end of the US Agency-MBS market – this is not the kind of investment you heard about during the financial crisis, or perhaps came across in the film The Big Short. This is quality-controlled in terms of the standards of the underlying home stock and in regards to the credit-score of individual mortgage holders. We’ve also subjected this investment to our own usual rigorous levels of analysis – find out more about how we choose our ETFs.

We reduced our exposure to short term government bonds in favour of US mortgage backed securities in portfolios because we believe MBS provides more attractive yields relative to government bonds, alongside diversifying fixed income exposure.

As always, our expert team will be closely watching the US mortgage backed security market as part of our wider investment strategy and managing the risk in our customers’ portfolios accordingly.

Sources

- SIFMA (Securities Industry and Financial Markets Association) 2020

- U.S. Securities and Exchange Commission – https://www.sec.gov/fast-answers/answersmortgagesecuritieshtm.html

- Bloomberg 2020

Risk warning

As with all investing, your capital is at risk. The value of your portfolio with Nutmeg can go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future performance.